Charting Receipt Automation Pathways: Custom Settings Powering History Logs and Transfer Verifications in Daily Finance Platforms

Receipt automation pathways have become central features in daily finance platforms as users manage increasing volumes of digital transactions across multiple accounts and services. These pathways rely on custom settings that users configure to dictate how receipts are captured, processed, and stored while connecting directly to history logs for accurate record keeping. In May 2026 many platforms expanded these capabilities through updated interfaces that allow finer control over data flows without requiring manual intervention at every step.

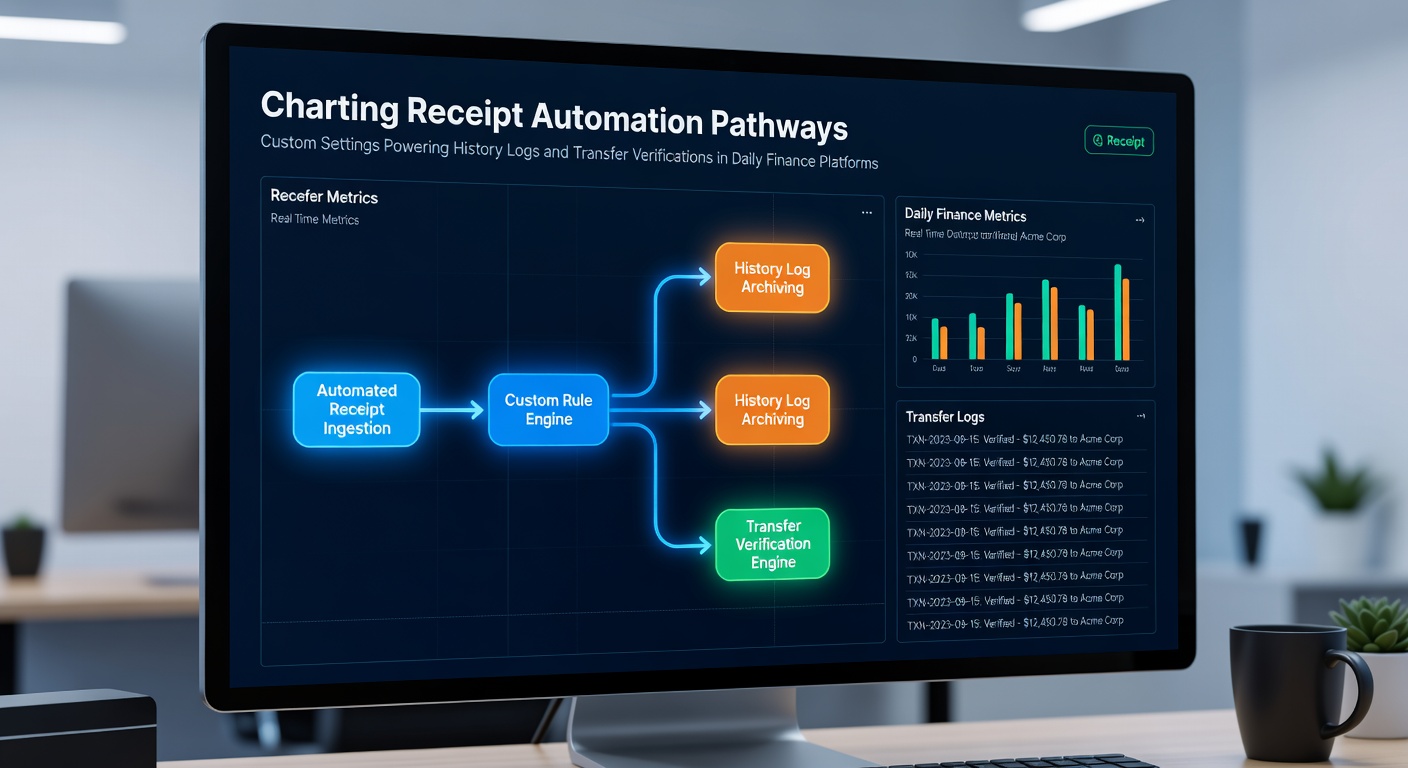

Mapping the Core Components of Automation Pathways

Automation pathways operate as sequential processes where receipt data enters the system through mobile scans or email integrations and then follows rules established in custom settings menus. Custom settings determine factors such as categorization tags, retention periods, and notification triggers that route information into centralized history logs. Observers note that these logs maintain chronological entries complete with timestamps, amounts, and merchant details, which support later verification of transfers by matching outgoing payments against corresponding receipt records.

Platforms achieve this integration by linking receipt metadata directly to transfer records through automated matching algorithms. When a user sets preferences for specific account types or transaction thresholds, the system applies those filters consistently across all incoming data. Research from the European Central Bank shows that such structured pathways reduce discrepancies in payment histories by up to 40 percent in tested environments.

Custom Settings as Control Mechanisms

Users access custom settings panels to define parameters that govern every stage of receipt handling. These options include selection of file formats for storage, assignment of approval workflows, and establishment of cross-references between receipts and bank transfer confirmations. Once configured, the settings operate continuously in the background, pulling data from connected financial institutions and populating history logs with verified entries. Experts have observed that granular controls allow organizations to tailor automation levels according to their reporting requirements, whether for personal budgeting or corporate expense tracking.

Integration with History Logs

History logs function as the central repository where automated pathways deposit processed information. Custom settings influence log structure by specifying which fields receive priority indexing and how duplicate entries receive resolution. When a receipt arrives, the pathway routes it through validation checks before committing the details to the log, ensuring that subsequent transfer verifications can query the data efficiently. Data from academic studies at the University of Toronto indicates that platforms using advanced log indexing complete verification tasks in roughly half the time compared with manual review methods.

Verification steps occur when the system cross-checks transfer amounts and dates against logged receipt values. Custom settings can activate alerts if mismatches exceed defined tolerances, prompting users to review specific entries. This process maintains data integrity across daily operations while supporting compliance needs in regulated financial environments.

Transfer Verifications Through Automated Pathways

Transfer verifications rely on the same custom configurations that manage receipt intake. Users establish rules that flag transfers lacking associated receipts or that require secondary confirmation before final approval. Pathways then generate audit trails within history logs, documenting every verification outcome for future reference. Those who have implemented these features report smoother reconciliation cycles because the automation identifies gaps early in the sequence rather than after month-end reporting.

Platforms continue to refine these verification mechanisms by incorporating machine learning elements that adapt to user patterns over time. As of May 2026 several providers introduced options to import external verification data from third-party services, expanding the scope of what history logs can capture without additional manual uploads.

Practical Implementation Across Finance Platforms

Daily finance platforms apply these pathways in both consumer and business contexts. Personal banking applications often emphasize simple toggles for receipt retention and basic transfer matching, while enterprise solutions offer layered permission systems that restrict who can modify custom settings. Regardless of scale, the underlying architecture remains consistent: settings direct data movement, logs preserve the results, and verifications confirm accuracy at each transfer point.

Industry reports highlight steady adoption rates as organizations seek to minimize errors in payment processing. The pathways reduce reliance on paper documentation and accelerate access to historical records when audits or disputes arise.

Conclusion

Receipt automation pathways supported by custom settings deliver structured approaches to managing history logs and transfer verifications in daily finance platforms. These systems process data through defined sequences that maintain consistency and support accurate record retrieval. Continued updates through 2026 reflect ongoing efforts to align automation tools with evolving user needs and regulatory expectations.