Configuration Choices Shaping Verification Accuracy Across Digital Remittance Networks

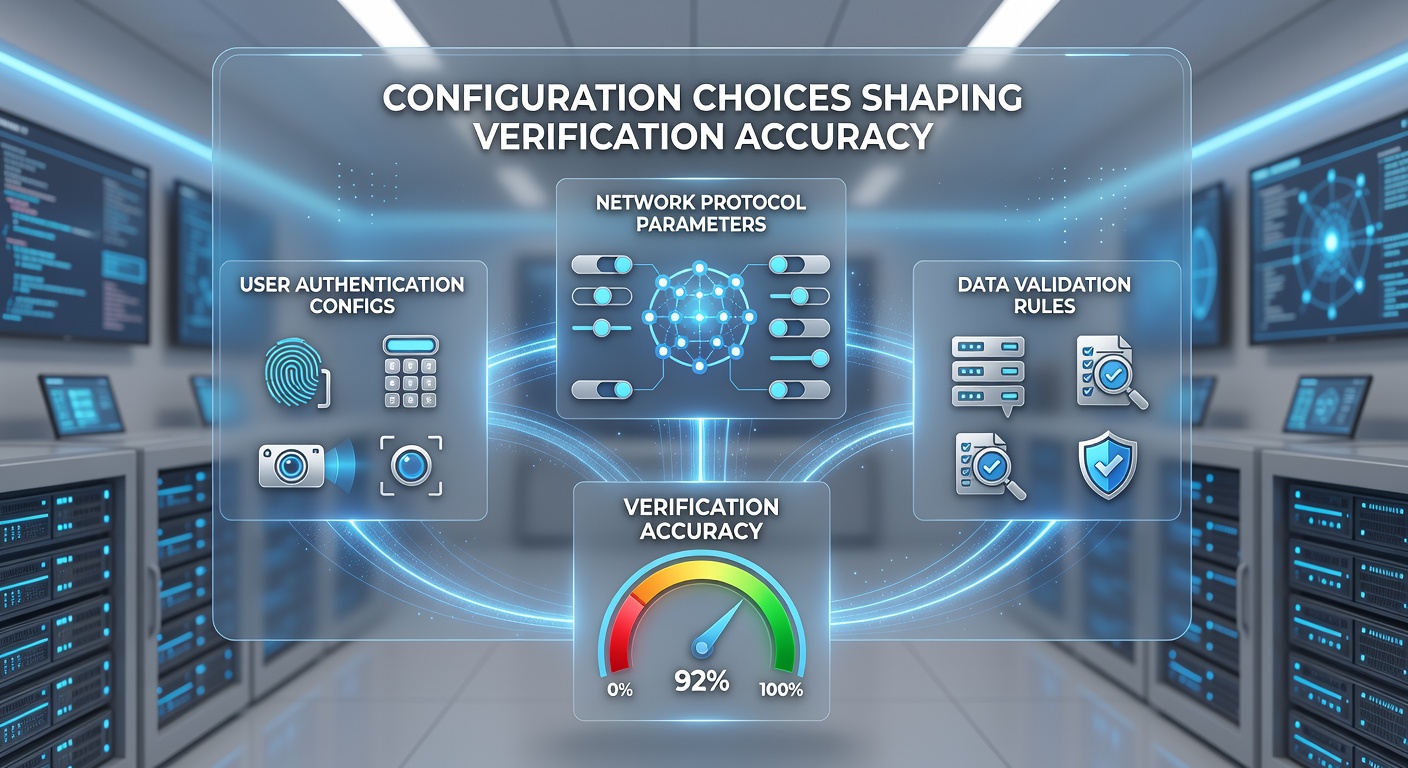

Digital remittance networks rely on specific configuration choices that determine how verification processes handle transaction data, identity checks, and compliance requirements. These settings influence error rates during cross-border transfers, where operators adjust thresholds for matching algorithms and data validation rules. According to reports from the Bank for International Settlements, precise tuning of these parameters reduces mismatches in recipient details while maintaining throughput across high-volume corridors.

Operators select between rule-based filters and machine learning models for initial screening. Rule-based systems apply fixed criteria such as name similarity scores or address format requirements, whereas adaptive models recalibrate based on historical patterns from previous transfers. Research from the European Central Bank indicates that hybrid approaches combining both methods achieve lower false positive rates in verification outcomes, particularly when networks process remittances involving multiple currencies and regulatory jurisdictions.

Parameter Thresholds in Identity Matching

Verification accuracy depends heavily on adjustable thresholds within identity matching engines. Networks set minimum similarity percentages for fuzzy matching of names, dates of birth, and identification numbers. Raising these thresholds tightens scrutiny and catches subtle discrepancies, yet it can also flag legitimate transactions that contain minor formatting variations common in international documents. Data compiled by the Reserve Bank of Australia shows that networks operating in the Asia-Pacific region often calibrate these values differently from those serving Latin American corridors due to variations in naming conventions and document standards.

Additional configurations cover document upload requirements and expiration date validations. Some platforms mandate supplementary fields like secondary identification numbers or source of funds declarations only when risk scores exceed predefined limits. These conditional triggers allow systems to allocate computational resources efficiently while directing human review toward higher-risk cases.

Integration Settings with External Data Sources

Remittance platforms connect to external databases for real-time checks against sanctions lists and credit bureaus. Configuration choices here include update frequencies for synchronized data feeds and fallback procedures during connectivity interruptions. Networks that poll sources every few minutes maintain fresher records compared to those using hourly batches, which affects how quickly new restrictions appear in active verifications. Figures from the World Bank highlight that delays in these integrations correlate with temporary spikes in declined transfers during periods of regulatory updates.

API timeout settings and retry logic also shape outcomes. Shorter timeouts prevent stalled processes but risk incomplete checks, while extended windows allow fuller responses at the cost of slower overall processing. Observers note that networks handling seasonal volume increases around holidays often modify these parameters dynamically to balance speed and completeness.

Regional Adaptations and Compliance Layers

Configuration frameworks accommodate regional regulations through modular rule sets. A network serving both European and North American users applies different address verification formats and tax identification requirements based on the destination country selected during transfer initiation. This segmentation prevents uniform rules from generating unnecessary rejections in one market while overlooking requirements in another.

June 2026 marks the scheduled implementation of updated messaging standards across several major remittance providers, which will require reconfiguration of field mapping and validation sequences. These changes aim to align data structures more closely with emerging global guidelines on payment messaging, potentially altering how verification engines parse incoming transaction details.

Monitoring and Adjustment Protocols

Continuous monitoring dashboards track verification success metrics such as approval rates, manual review volumes, and reversal frequencies. Operators review these indicators weekly or monthly to decide whether threshold adjustments are necessary. Automated alerts notify teams when accuracy metrics fall outside expected ranges, prompting targeted reviews of specific configuration values rather than broad system overhauls.

Case studies from networks operating in Africa demonstrate how localized adjustments to phone number format validation improved match rates for recipients using mobile money services. Similar refinements applied to postal code fields in Canadian corridors produced measurable reductions in processing exceptions without increasing overall risk exposure.

Conclusion

Configuration choices across digital remittance networks directly determine verification accuracy through their effects on matching logic, data integration, and regulatory compliance layers. Networks that document and periodically reassess these settings maintain consistent performance as transaction volumes and regulatory landscapes evolve. The interplay between technical parameters and operational needs continues to guide how platforms refine their verification processes over time.