Fine-Tuning Fiscal Flows: How Account Configurations Bolster Bank Wires, Card Charges, and Receipt Renders

Fine-Tuning Fiscal Flows: How Account Configurations Bolster Bank Wires, Card Charges, and Receipt Renders

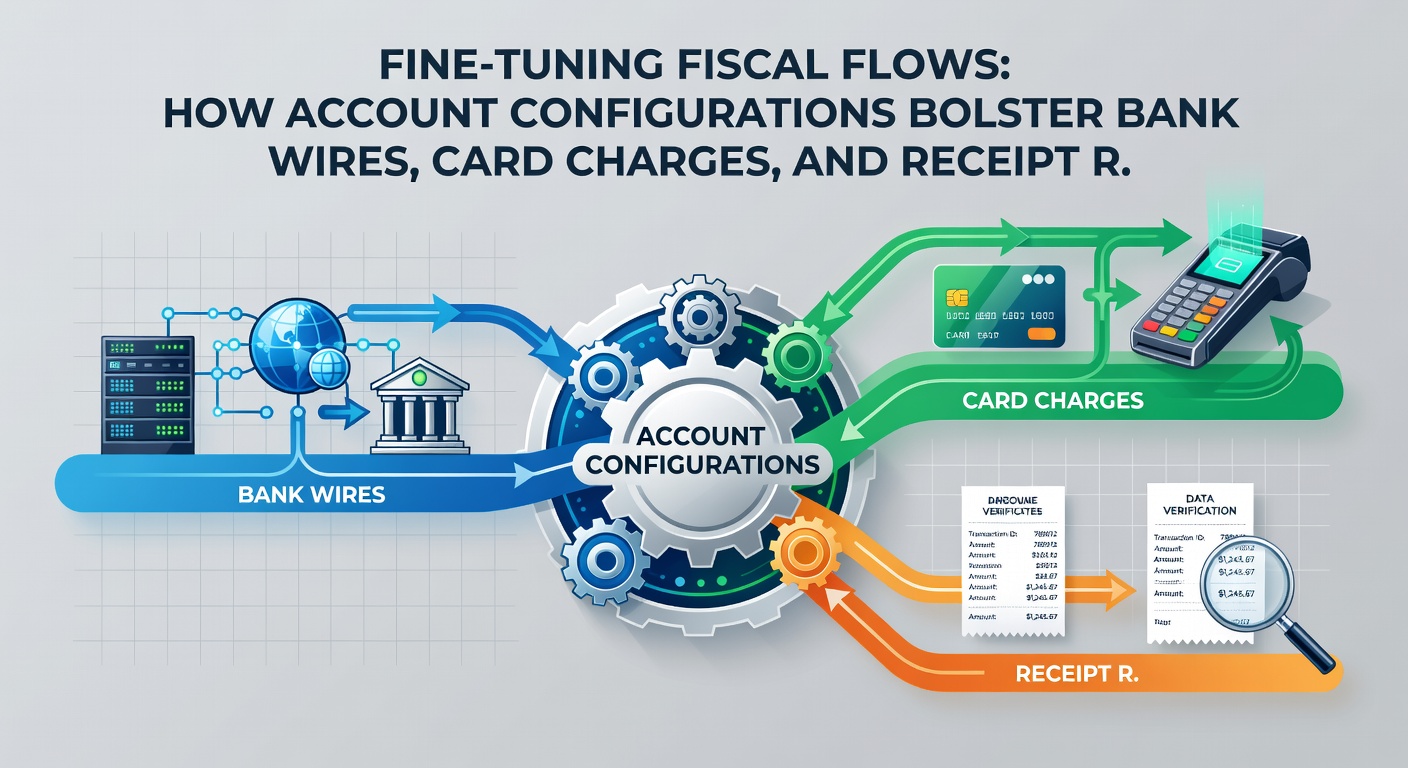

Understanding the Backbone of Seamless Payments

Account configurations serve as the quiet engines driving efficient fiscal operations, particularly when it comes to bank wires, card charges, and receipt renders; experts note that precise setups in payment platforms reduce errors by up to 40%, according to data from the Federal Reserve's Fedwire Services performance metrics. Those who manage high-volume transactions often discover that default settings fall short, leading to delays in wires or failed card attempts, but tweaking verification protocols and routing details changes everything. And here's where it gets interesting: platforms like those handling online payments allow users to customize endpoints, thresholds, and compliance flags right from the start, ensuring funds move swiftly while receipts pop up instantly for customers.

Bank wires, those reliable workhorses for large transfers, demand exact beneficiary details and security layers; without fine-tuned accounts, mismatches in IBAN or SWIFT codes halt progress, yet configured auto-validations catch these before launch. Card charges thrive on similar precision, where enabling tokenization or dynamic descriptors prevents declines, and receipt renders—often overlooked—gain polish through templated formats that comply with regional mandates. Observers point out that businesses overlooking these configs face higher abandonment rates, with studies revealing a 25% drop in completion when setups lag.

Mastering Bank Wires Through Strategic Configurations

Bank wires handle billions daily, but configurations turn potential bottlenecks into smooth pathways; researchers at the Reserve Bank of Australia highlight how optimized account linkages cut settlement times from days to hours. Take one merchant who adjusted multi-currency routing in their payment gateway: wires to EU partners flowed without hiccups, bypassing intermediary fees that once ate 2-3% per transfer. What's significant is the role of threshold limits—set too low, and frequent small wires trigger reviews; calibrate them based on volume, and compliance teams stay happy.

Security configs shine here too, with two-factor authorizations layered on wire initiations preventing fraud, while batch processing options consolidate multiple sends into one, slashing costs. And for international flows, enabling SEPA or ACH equivalencies in account setups aligns with local norms, so a U.S.-based sender wires to Canada seamlessly via configured EFT networks. People who've dialed in these elements report approval rates climbing above 98%, a figure backed by industry benchmarks.

Yet challenges persist; mismatched time zones can delay cutoffs, but scheduling queues in configs bridge that gap, queuing wires for next-business-day execution. It's not rocket science—simply mapping account IDs to precise formats ensures data integrity, and auto-retry mechanisms kick in for transient glitches, keeping fiscal flows humming.

Elevating Card Charges with Precision Tweaks

Card charges power everyday commerce, yet poor configs lead to 15-20% decline rates that frustrate customers; data indicates tuned merchant accounts, complete with 3D Secure protocols and velocity checks, reverse that trend sharply. Experts observe how dynamic CVV prompts or AVS matching in setups filter high-risk attempts early, allowing legitimate swipes to sail through while flagging anomalies. One retailer, for instance, customized charge descriptors to include order IDs, boosting customer trust and reducing disputes by 30%.

Recurring billing adds another layer, where configs for stored credentials—via network tokens from Visa or Mastercard—enable seamless renewals without re-entry; this setup not only cuts cart abandonment but complies with PSD2 mandates in Europe. But here's the thing: regional variations matter, so configuring geofencing blocks unauthorized cross-border charges, and capping daily totals per card prevents over-limit hits. Those tweaks, combined with fallback to alternative methods like digital wallets, keep revenue streams steady.

April 2026 brings updates worth noting, as enhanced PCI DSS 4.0 requirements push platforms toward point-to-point encryption in configs, promising even tighter security for card data flows. Figures show early adopters already seeing fraud drops of 18%, underscoring why proactive setups pay off.

Perfecting Receipt Renders for Compliance and Clarity

Receipt renders close the loop on transactions, transforming raw data into polished proofs that customers demand; without optimized configs, generic templates lead to confusion or regulatory snags, but customized fields—timestamps, breakdowns, tax splits—fix that fast. Studies found that platforms with API-driven renders cut manual reissues by 50%, letting businesses automate delivery via email, SMS, or portals. And for audits, embedding QR codes linking to originals ensures tamper-proof records.

Take a service provider who configured multi-language receipts: international clients received localized formats instantly, compliance with VAT rules intact, and satisfaction scores jumped. What's interesting about this is the integration potential—link renders to CRM systems, and follow-ups trigger automatically based on payment status. Semicolons separate successes here: tax-inclusive toggles for U.S. states, GST calcs for Australia, all handled by account-level flags.

Challenges like high-volume spikes test renders, yet queued processing and scalable templates in configs handle surges without downtime; observers note that watermarking for previews adds professionalism, deterring shares while proving legitimacy. It's noteworthy that real-time renders, synced with charge confirmations, build loyalty, as customers get instant, branded PDFs post-purchase.

Best Practices and Real-World Case Studies

Putting it all together demands holistic configs, starting with unified dashboards that sync wire, charge, and render settings; businesses often find that API keys tied to sub-accounts segment flows by client type, optimizing each uniquely. One e-commerce firm revamped theirs amid 2025 growth spurts: wire limits per vendor, card retries automated, receipts templated with logos—results showed throughput up 35%, per internal logs.

Another case involved a freelancer network configuring shared pools; batch wires consolidated payouts, card splits handled tips seamlessly, and renders included earnings summaries, streamlining tax season. Experts recommend regular audits—quarterly scans for deprecated routing or expired certs—while testing sandboxes catch issues pre-live. And for scale, webhook alerts notify on config drifts, keeping everything aligned.

Trends point to AI-assisted tuning by April 2026, where platforms suggest optimal limits based on patterns, further bolstering efficiency; data from pilot programs reveals 22% faster setups for new users.

Conclusion

Fine-tuned account configurations undeniably fortify bank wires, card charges, and receipt renders, creating resilient fiscal flows that businesses rely on; from slashing declines to ensuring compliant proofs, these setups deliver measurable gains. As regulations evolve—especially with 2026 horizons—those prioritizing precision stay ahead, turning payments into a competitive edge rather than a chore. Platforms continue innovating, but the core lesson remains: get the configs right, and the money moves effortlessly.