How Customized Configurations Strengthen Credit Processing and Document Automation Across Banking Systems

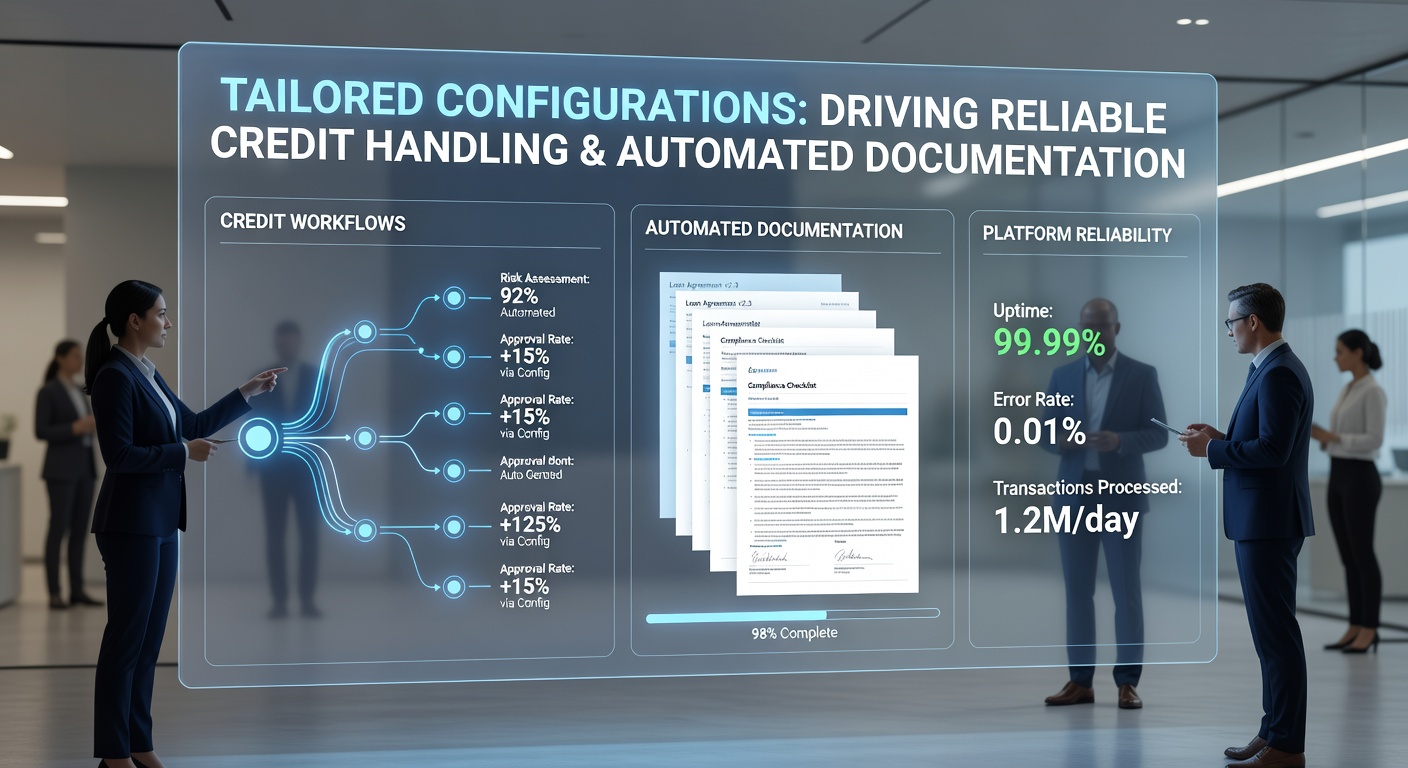

Banking platforms rely on carefully adjusted settings to manage credit transactions with precision while generating required records without manual intervention. These adjustments allow institutions to align system behavior with specific operational needs, regulatory demands, and client profiles, which reduces processing delays and limits discrepancies in financial records. Observers note that institutions which implement detailed configuration layers often see measurable improvements in both transaction accuracy and compliance reporting. Data from recent industry analyses show that platforms using modular rule sets complete credit approvals faster and maintain clearer audit trails compared with those relying on default parameters.

Banking platforms rely on carefully adjusted settings to manage credit transactions with precision while generating required records without manual intervention. These adjustments allow institutions to align system behavior with specific operational needs, regulatory demands, and client profiles, which reduces processing delays and limits discrepancies in financial records. Observers note that institutions which implement detailed configuration layers often see measurable improvements in both transaction accuracy and compliance reporting. Data from recent industry analyses show that platforms using modular rule sets complete credit approvals faster and maintain clearer audit trails compared with those relying on default parameters.Core Elements of Configuration Design in Credit Workflows

Tailored setups begin with defining parameters for risk assessment, approval thresholds, and repayment schedules. System administrators establish rules that determine how incoming credit requests are evaluated against internal policies and external credit data sources. When these rules incorporate client-specific variables such as account history and transaction patterns, the platform routes requests through appropriate verification steps automatically.

Studies from financial technology research groups indicate that configurable credit engines decrease manual review rates by up to thirty percent in mid-sized banks. This occurs because the system applies consistent logic across similar cases while still allowing exceptions to be flagged for human oversight only when predefined conditions are met.

Supporting Automated Documentation Through Rule-Based Triggers

Automated record creation depends on triggers that activate whenever a credit event occurs. These triggers pull relevant data fields, apply formatting standards, and store outputs in designated repositories. Institutions configure document templates to include required disclosures, signature fields, and regulatory notices so that each generated file meets current standards without additional editing.

What's notable is how these same triggers also populate compliance logs that regulators review during examinations. The European Banking Authority has published guidance showing that banks using automated documentation systems report fewer omissions in required filings, particularly when configuration updates are synchronized with changes in reporting deadlines.

Integration With Existing Infrastructure and Regulatory Updates

Effective configurations must connect smoothly with core banking systems, payment processors, and external data providers. Developers achieve this by mapping data fields across platforms and setting validation checks that run before any record is finalized. In May 2026, several major institutions completed platform upgrades that incorporated new data privacy rules from the Australian Securities and Investments Commission, demonstrating how configuration layers can accommodate regional regulatory shifts without full system replacements.

Researchers at the Bank for International Settlements have documented cases where banks reduced reconciliation errors by configuring automated cross-checks between credit ledgers and general accounting modules. These checks run at scheduled intervals and generate exception reports that compliance teams review, which keeps operational costs contained while maintaining record integrity.

Practical Outcomes Observed in Deployed Systems

Take one regional bank that adjusted its credit handling parameters to reflect seasonal cash-flow patterns common among agricultural clients. The updated rules allowed the platform to apply flexible repayment schedules automatically and produce corresponding amortization schedules as part of the standard documentation package. Staff reported that loan officers spent less time correcting paperwork and more time discussing client needs.

Similar results appear in platforms serving commercial lending, where configuration sets control interest accrual methods, collateral tracking, and covenant monitoring. When these elements operate under unified rules, the system produces consolidated reports that satisfy both internal management and external auditors.

Looking Ahead to Continued Refinement

As platforms evolve, configuration tools are expected to incorporate more granular controls over machine learning models used in credit scoring. Institutions continue to test how adjustments to model weights and feature selection affect approval rates and default predictions while preserving explainability requirements. Ongoing work in this area focuses on maintaining transparency so that automated decisions remain reviewable and defensible under current oversight frameworks.

Conclusion

Tailored configurations serve as the operational backbone that enables banking platforms to handle credit requests reliably and produce documentation consistently. By aligning system rules with business requirements and regulatory expectations, institutions achieve faster processing cycles and stronger audit readiness. Continued attention to these settings will remain central as platforms adapt to new data sources and compliance obligations in the years ahead.